YOUR BUSINESS AUTHORITY

Springfield, MO

YOUR BUSINESS AUTHORITY

Springfield, MO

Last edited 10:57 a.m., Aug. 20, 2020

Among its vast economic impacts, the coronavirus pandemic is moving customers out of local bank lobbies and toward online and mobile banking alternatives.

Local banking officials say many customers are either utilizing digital banking for the first time this year or expanding their access, as lobbies temporarily shuttered to walk-in traffic in March. Several months later, access inside some banks remains limited as a safety measure for employees and visitors.

Lobby customer traffic has been quiet at Springfield First Community Bank, said CEO Rob Fulp. Customers are welcome by appointment only inside the bank’s lone branch at 2006 S. Glenstone Ave. Masks are required and social distancing is in place with areas roped off inside to guide customers.

Meanwhile, Fulp said SFC’s online and mobile usage is tracking high over the past 90 days. Mobile deposits are up 25%, while mobile and online banking users have grown 18% and 14%, respectively.

“It’s not about brick-and-mortar anymore. It’s about technology and talent,” he said. “The focus we’ll have going forward is to continue to enhance technology, because it’s going to change.”

Financial services research firm Novantas found in a June study that year-over-year U.S. bank branch traffic fell over 30% in April and the first three weeks of May. Teller transactions dropped 32% in March and April over the same period in 2019.

At the same time, the increase in U.S. mobile banking is contributing to a market on the verge of exploding globally. A March report from Allied Market Research projected the global mobile banking market size will hit $1.82 billion by 2026, up from an estimated $715.3 million in 2018.

Making an investment

The focus on technology is top of mind for Simmons First National Corp. (Nasdaq: SFNC), said Alex Carriles, executive vice president and chief digital officer. The regional bank invested around $100 million last year in a yearlong technology initiative dubbed Next Generation Bank, which included a new mobile app. The Pine Bluff, Arkansas-based company operates five Springfield branches.

Carriles said roughly 30% of lobbies for the bank’s 200 branches in seven states are currently open, with the remainder drive-thru only.

“We already had pretty much all of our customers on our new mobile banking platform,” he said of the bank’s digital efforts prior to the pandemic.

The investment is paying off. From March through June, Simmons Bank’s digital users jumped 23%, with a 28% increase for digital transactions, Carriles said, declining to disclose user and transaction totals.

“Not only did we have more users, but the users that we had were using even more of the digital platform,” he said. “We are making some changes to our mobile deposit platform, given the volume and adoption we’re seeing, to increase the limits in the future and make the process easier and faster.”

Technology investments by banks are essential now, said Jackson Hataway, senior vice president of communications, marketing and member services with the Missouri Bankers Association.

“Apps were not a thing in banking until about 10 years ago. Suddenly, you had to have an app and had to have mobile and web capabilities and online banking,” he said. “We expected and saw more consumers become comfortable with that across demographics.”

Carriles said in general bank branches, while still important, will serve a different purpose in the future than just a place to execute transactions. They should be somewhere people go for advice, learn about products and find ways to improve finances, he said.

“Focus on those things that the customer prefers to do face to face,” he said.

Shedding branches

Simmons Bank plans to close its 4021 S. Campbell Ave. branch in Springfield and its lone Greenfield location in October. Officials cite customers’ increased use of mobile and online banking as a contributing factor.

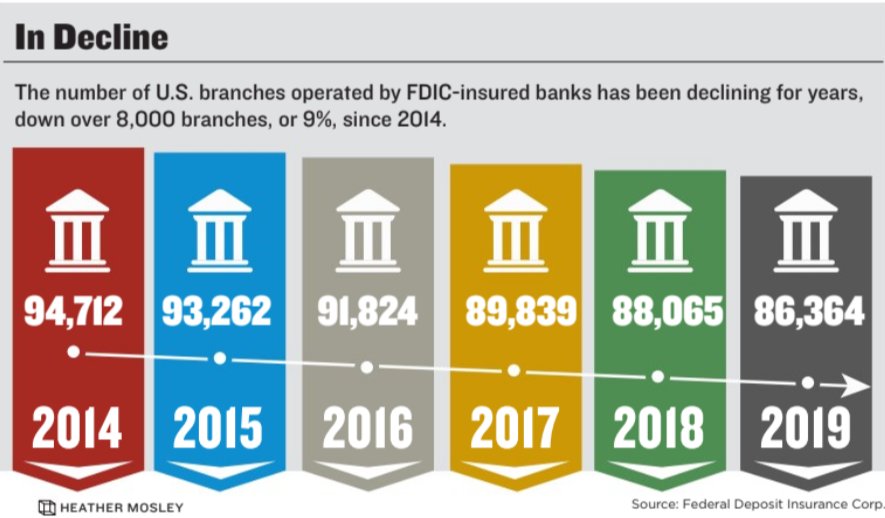

The decision is hardly an isolated incident. According to the Federal Deposit Insurance Corp., the number of U.S. branches operated by FDIC-insured banks has been on the decline well before the pandemic, dropping 8,348, or 9%, since 2014.

The industry’s largest banks are not immune to the branch shedding. According to a March study by financial data tracking firm SmartAsset, three of the top five U.S. banks, JPMorgan Chase (NYSE: JPM), Bank of America (NYSE: BAC) and Citibank (NYSE: C), closed locations at an average pace of 7%. The study further reported 49 of the 50 largest cities in the country recorded a decline in bank branches between 2014 and 2018.

Even as branch counts are dropping, domestic deposits held by FDIC-insured institutions increased 4% to $12.77 trillion in June 2019 from $12.26 trillion a year prior.

There’s been a national 2% decline in branches year-over-year for the past several years, Hataway said. In Missouri, the decline is around 3.2% over the last five years. However, banking officials say it’s too early to tell if a drop this year in walk-in traffic translates to long-term impact.

“It is possible COVID-19 will accelerate that trend to some degree, given the uptick in digital products and services, but there’s not data yet to indicate that will happen,” Hataway said.

Despite the decreasing trends in bank offices, new branch investment is part of Mid-Missouri Bank’s plan in 2020. In October, the bank is scheduled to open a new $4 million, three-story headquarters at 1619 E. Independence St., said spokesperson Andrew Moore. The project includes a 3,000-square-foot, full-service bank on the first floor. Mid-Missouri Bank operates 13 facilities in 10 communities.

“We’re actually investing more in our facilities and it’s a strategy of ours moving forward,” he said. “That really has to do with offering everything that is new and available, but not taking away anything that our customers might prefer or be used to.”

SFC’s Fulp said his bank also is looking to add another branch, with a location announcement likely next year. SFC is owned by Moline, Illinois-based QCR Holdings Inc. (Nasdaq: QCRH).

Branches will continue to decline nationally as customer expectations in technology continue, he said. It’s important to meet consumer needs no matter the space in which they bank, he said, or if their accounts are commercial or retail. For Fulp, it comes down to relationships.

“In the future, online technology is going to win, but there will always be a place for walk-in lobby traffic here at this bank. That’s kind of our culture,” he said. “It just might not be what it’s been in the past.”

Moore said physical banks likely would never go away entirely.

“Some people want to see the person that they’re trusting with their money,” he said.

Missouri State University’s science building, built in 1971 and formerly called Temple Hall, is being reconstructed and updated.