YOUR BUSINESS AUTHORITY

Springfield, MO

YOUR BUSINESS AUTHORITY

Springfield, MO

A Murney Associates email broke the news: Median home prices in the Ozarks peaked at $270,000 in May, a record for the region.

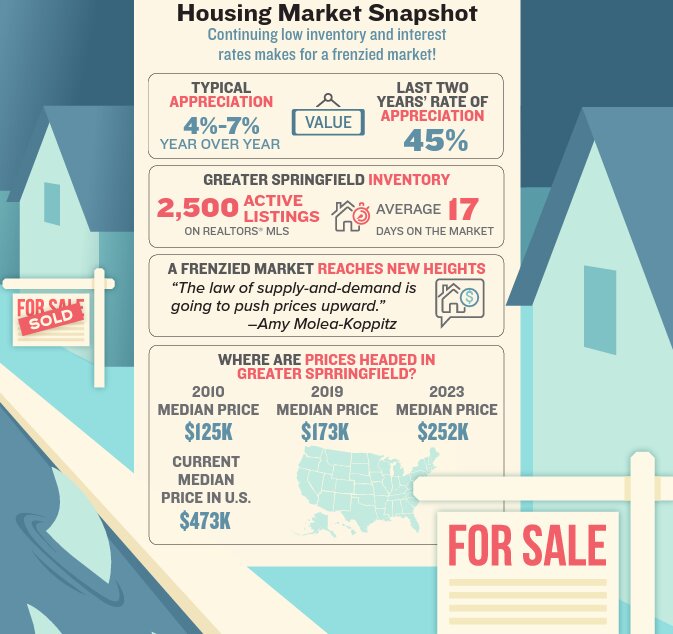

“With mortgage rates hovering around 6% and housing inventory remaining low, we’re expecting a fairly stable market throughout the summer,” Realtor Bill Abbott reported.

Jeff Parker, managing broker for Murney Associates, Realtors, confirmed that home prices have broken a record locally.

“Inventory has climbed, but just slightly,” he said. “It hasn’t been enough to affect prices, and honestly, I’m not sure if prices would be affected.”

Pricing in the Springfield area has been behind, Parker said, and the recent adjustment was a market correction.

“Our labor market has been cheaper. That’s gone up. The entire economy and higher prices have taken a long time to get to the Ozarks,” he said.

For a long time, the region had some of the lowest real estate prices in the country, he said.

“We still have the affordability factor compared to other areas, but the days of $150,000 three-bed, two-bath, two-car garage have gone by the wayside,” he said. “I don’t think they’ll ever return.”

Equity at play

Amy Molea-Koppitz is an agent with Keller Williams Greater Springfield. She said real estate prices are constantly on the rise.

“Over any 10-year period that you look at, if you buy property and hang onto it and think long-term, it’s always a good investment,” she said.

She suggested that potential first-time homebuyers not be daunted by the rise in prices.

“They should start having that conversation with some advisers – how do I get to that place where I become a homeowner?” she said. “There are options, but it may take some thinking outside of the box.”

Molea-Koppitz said home prices are higher across the board.

“This year we’re seeing the number of sales go down a little bit, but we’re not seeing a decline in price because there’s such a shortage in inventory,” she said.

She said the current median sales price for the five-county Springfield metropolitan statistical area is $251,732, based on Keller Williams’ multiple listing service data.

By comparison, immediately before the pandemic, in 2019, the median price was $173,300.

“In a short period of time, we’re seeing a pretty significant gain in equity,” she said.

In other words, the real estate train has picked up steam, which is good news to its passengers, but not to someone wanting to hop on.

Molea-Koppitz said when she moved to Springfield in 2010, colleagues told her Springfield is its own little bubble, and while she shouldn’t expect massive price gains year over year, she could anticipate a consistent 5%-10% gain. At the time, the median sales price in the Springfield MSA was $125,000 – about half its current level, according to Molea-Koppitz.

The pandemic brought a change, however, with out-of-state buyers paying cash for properties and driving up values in the area.

The Federal Reserve Bank of St. Louis reports the current median home value in the United States is $437,000.

“To us, the prices here feel high based on all we’ve seen and known for this area,” Molea-Koppitz said. “Looking at the nation as a whole, we’re still much cheaper.”

She said people now can work remotely from anywhere, and a recent article in The Wall Street Journal singled out Springfield as the best place in the country to do just that.

She noted buyers from other states, particularly California, often report they want to get away from heavy taxation and government overreach to what they report is the relative freedom of the Show-Me State.

“I would say we get a large influx of buyers from California, Arizona, Texas,” she said. “Things are getting so expensive, people are just priced out of homeownership. They can come here and still afford to buy a home.”

Those outside pressures result in local prices rising, she said.

“If you have low inventory – and we don’t have a ton of homes on the market – and you have increased buyer demand, including people from other states, the law of supply-and-demand is going to push prices upward.”

Jeff Kester is CEO of the Greater Springfield Board of Realtors. In 2016, he was board president for the organization. At that time, he said, there were around 6,000 active residential listings in the Springfield metropolitan area. Right now, the inventory is at 2,500, and it has been as low as 1,700 recently.

“That’s an amazing difference,” he said. “In 2016, we had about seven months of inventory; right now we’ve got about two, but it’s been as low as a month and a half.”

Usually, Springfield homes average 30 days on the market in warm-weather months and 60 days in the winter. In the last two years, average days on market have stayed around 10 days or less, he said.

“As of May, average days on market is back down again, sitting about 17,” Kester said.

Rising prices have accompanied the trend.

Greene County residents recently received notifications from the Assessor’s office informing them of changes in their property values, most of which have risen.

“In the past two years, Greene County has had a substantial increase in the residential real estate market,” a May news release from the assessor stated. “Some of the contributing factors include high demand and low supply, recovery from COVID, purchases by real estate investment companies, low interest rates, and the high desirability to relocate to the Springfield metropolitan area.”

An inventory issue

Kester agreed with Parker and Molea-Koppitz that the higher home values are all about inventory.

“There just aren’t enough homes,” he said.

New houses are being built, Kester said, but the inventory is not in categories that would move more people through the market.

Complicating matters is the fact that interest rates are higher – 6.7% on average nationally for a 30-year fixed rate mortgage, according to the St. Louis Fed. Those who bought a house at 3% or 4% may be reluctant to move to a home at a higher rate.

Kester said Springfield is low on options like condominiums and townhomes.

“That’s just not historically been a thing we do here in Springfield, for a lot of reasons,” he said. “That single-family detached ranch home is by far, culturally, what everybody wants – their piece of ground, detached from everyone else.”

Kester said when he and his wife bought their house in the 1990s, a lot of starter homes were being built, and theirs was priced in the mid $60,000s.

“Now, it’s in the high $100,000s,” he said.

“If you’re someone who bought a house and kept owning it through the Great Recession, it’s not a housing crisis – it’s a housing boom,” he said. “You’ve seen your equity soar over time.”

On the contrary, the market feels very much like a crisis for someone looking to buy a first home or perhaps relocating from another market.”

When asked if he has any predictions for what the market will do, Kester joked that he had thrown away his crystal ball.

“In terms of advice, whether you are a regular buyer or an investor, I can’t imagine anyone trying to navigate the current housing environment without a qualified professional to help them through it because of all the things that go into a real estate transaction now,” he said.

“It has risen to an almost expert level; therefore you need an expert.”

The pool is full of alligators, Kester said.

“It has always been alligators, but the alligators have grown now, with so many things that go into lending and title work and inspections … I can’t imagine,” he said.

Moseley’s Discount Office Products was purchased; Side Chick opened in Branson; and the Springfield franchise store of NoBaked Cookie Dough changed ownership.