YOUR BUSINESS AUTHORITY

Springfield, MO

YOUR BUSINESS AUTHORITY

Springfield, MO

In the summer of 2017, Patricia Reynolds received a large utility bill.

Unable to make the payment, she acquired a $300 short-term payday loan.

“I kind of got locked into it,” Reynolds said. “I thought when I did it I could pay it off, but they told me you could pay the interest and keep the loan going, not realizing how much interest was going for that.”

Paying about $52 a month to cover interest was all Reynolds could afford, and she continued to renew the loan until she accrued $1,300 worth of interest debt.

Stories like Reynolds’ have sparked bills in the Missouri House of Representatives and a subcommittee led by Rep. Steve Helms, R-Springfield, which investigated potential problems with short-term loans.

The bills

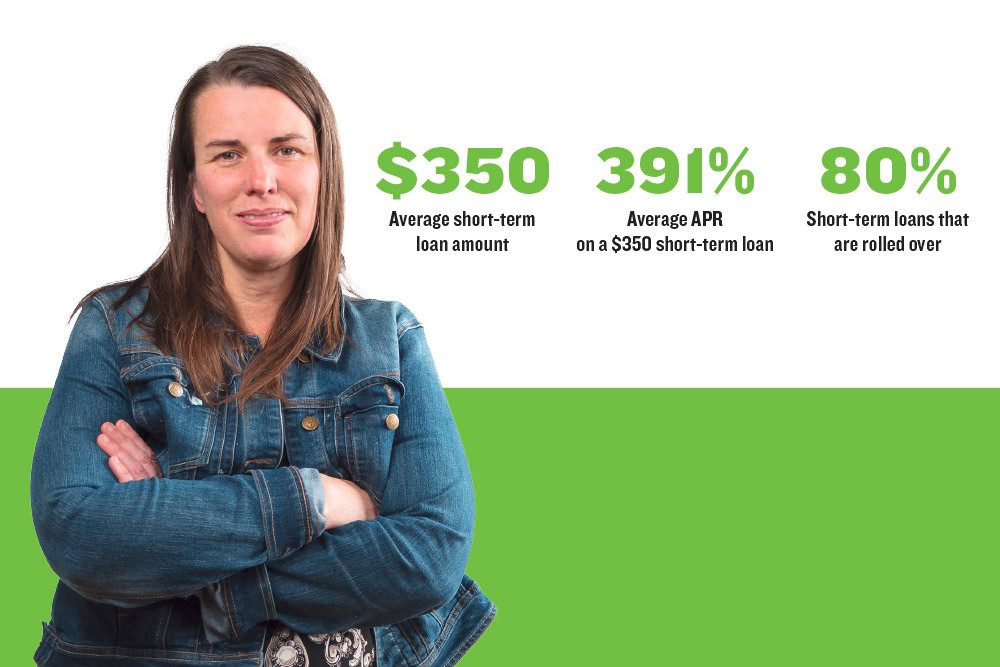

According to the Consumer Federation of America, the maximum short-term loan amount permitted in Missouri is $500 with a term of 14-31 days. The average loan amount is $350, according to a 2016 analysis by the Consumer Financial Protection Bureau. Loans are permitted to renew, or roll over, no more than six times, and the principal loan amount must be reduced by 5 percent with each renewal. This results in an annual percentage rate of 391 percent on a $350 loan.

Because of this, in October 2017, the CFPB issued new rules requiring lenders to ensure consumers are able to repay payday loans and end renewal attempts. According to its analysis, more than 80 percent of payday loans were rolled over within 30 days of when the loan was first acquired. The rules, however, will not fully go into effect until August 2019.

In the meantime, Cheryl Clay isn’t waiting for federal changes, focusing rather on the local level. As National Association for the Advancement of Colored People Springfield chapter president and board member of Missouri Faith Voices Inc., Clay advocates for House Bill 1541 – sponsored by Rep. Lynn Morris, R-Nixa, with Rep. Crystal Quade, D-Springfield, as co-sponsor – which would reduce the APR to 36 percent. Rep. Martha Stevens, D-Columbia, sponsored HB-1932, which also would enforce a 36 percent cap.

The lack of an APR cap is the biggest difference in HB-2657, sponsored by Helms. It’s also why Helms said his bill has already had a public hearing.

“There is no way that cap on the APR will pass the House and Senate,” he said. “It doesn’t matter what we want. That is just the mood, and I just don’t think it’s going to happen. My view is, let’s get something. Because we can argue and argue over the 36 percent APR and, if I were to include that in the bill, my bill would probably go nowhere.”

Morris, however, said about 11 other states have laws capping APR.

“It’s not impossible,” he said. “I don’t want to hurt their business; I’m just trying to help people.”

For Greene County Baptist Association Director Michael Haynes, the law changes are a moral issue. And although attaining an APR cap would be desirable, Haynes said he is eager for any changes.

“It’s really ridiculous and amazing that it’s not self-evident that this is wrong,” he said. “We’ve had people working in this area and trying to encourage legislatures to change this for a good while.”

APR battle

Helm’s lack of an APR rule has lost some support from community advocates.

“He’s trying to make the business community happy and the community happy, but until that interest rate is capped, he’s not going to make the community happy,” Clay said.

Missouri Faith Voices Congregational Coordinator Susan Schmalzbauer voiced support for Morris’ bill, while expressing concern regarding Helms’ lack of an APR cap.

“It does little to reform and help people get out of the debt trap,” she said.

On Oct. 3, 2016, the Military Lending Act put a 36 percent interest cap on most consumer loans – including short term – taken out by active-duty servicemembers and covered dependents, according to the CFPB.

“Why shouldn’t that be for everyone in our community?” Clay said. “If it’s so offensive for our military to be charged these rates, then I think it should be equally offensive for the poor in our community to be charged that rate, also.”

Helms said the CFPB’s new rules could create the 36 percent cap – however it is uncertain if those laws will go into effect under the President Donald Trump administration.

“They said they’d relook at those rules,” Helms said. “And they’re going to be making changes. At this time, no one has any idea what changes the federal government could do.”

With that backdrop, Helms said the House placed him in charge of the Subcommittee on Short Term Financial Transactions to evaluate the needs of both lenders and consumers.

“We didn’t look at anybody’s bill,” Helms said. “Our intention at our hearing was to talk to consumer folks, nonprofits, the payday lenders, banks, credit unions, Missouri Department of Finance, and get a general view of what the issues are out there. We wanted to look at it from a fresh approach.”

The subcommittee held three hearings in February and submitted its final report on March 1.

Although his bill does not include an APR cap, Helms said he believes it addresses the most grievous issues identified in the report: Reducing the limit of renewals to two times from six, and decreasing the interest and fees to 35 percent from 75 percent.

Helms said he is trying to schedule a hearing during the first week of April. Morris said he hopes his bill is assigned to a committee and is heard in at least one committee. With both a Democrat and Republican sponsoring the bill, Morris said he thinks it would have success on the floor.

“By having someone co-sponsor the same bill on both sides, we pull in all the Democrat votes and most of the Republican votes,” he said.

Another way

Based on subcommittee hearings, Helms said there were concerns an APR cap would put lenders out of business and that there would be no other market for consumers to receive short-term loans. Among states with an APR cap are North Carolina and Arkansas, Schmalzbauer said. Many short-term lenders left those states after the law went into effect, she said, and the others evolved.

“The ones that did were able to make a business model that worked and people were still able to get short-term loans,” she said. “Faith Voices is not anti-business. We believe people need access to fair credit.”

When Springfield Business Journal contacted several local short-term lenders, representatives referred questions to their corporate spokespeople, who did not return calls by press time.

Greene County Baptist Association’s Haynes said a low interest rate on short-term loans would not keep a lending company afloat.

“If they are just attracting people who are paying these loans off in 30 days, they aren’t going to make any money off of that,” he said. “They are depending on those who are not able to pay their loan off after one month. If it’s $350, the person has to pay $2,000 or $3,000 to get the loan paid off.”

For that reason, he calls the loans “predatory.”

In Springfield, CU Community Credit Union’s short-term loan equivalent, called “fresh start loans,” have a 26 percent APR and do not allow renewals.

“The outcome is wonderful,” CEO Judy Hadsall said. “I can’t tell you the difference it makes in people’s lives. They were so bogged down with payday loans and we were able to consolidate that and put them on a payment plan.”

Hadsall acknowledged there’s not much profit with only 26 percent APR. For lending companies with eggs all in the short-term loan basket, it won’t keep the lights on. Hadsall recommended those companies expand to include additional services, such as savings plans to work with borrowers after they pay off the loan.

That’s the heart of the issue, Hadsall said – and although it’s difficult to determine a cure-all, it’s one solution to end the cycle other than legislation.

“When people get into these short-term loans, they have a difficult time paying back in the term that is required to pay it back, and that’s when they get into the vicious cycle,” she said. “There is going to have to be more teeth into the bill if they truly want to try and change it.”

For the people

Stuck in a cycle of debt with $1,300 in interest accrued, Reynolds enrolled in University Heights Baptist Church’s University Hope program, which partners with local credit unions to help borrowers pay off short-term loans.

Today, she is $70 away from being debt-free.

Hadsall works with The Northwest Project to assist short-term loan borrowers in developing payment plans and savings accounts to prevent the need for future loans. However, the biggest roadblock in repeating success stories is the stigma of a short-term loan, Hadsall said. Often, the borrower is afraid to seek assistance.

“They are afraid people will look down on them and think, ‘Why did you do this?’ That we’re going to judge them,” she said. “It’s hard to get them to understand that we’re here to help and not judge or look down on them because of financial problems. By the grace of God, it could be you and I. It happens. Everyone has challenges in their lives, and we just want to help.”

Utah-based gourmet cookie chain Crumbl Cookies opened its first Springfield shop; interior design business Branson Upstaging LLC relocated; and Lauren Ashley Dance Center LLC added a second location.

Updated: Systematic Savings Bank to be acquired in $14M deal

Warby Parker store planned in Springfield

Former CoxHealth colleagues starting communications firm

Former Wentzville superintendent to get $1M in contract buyout

STL construction firm buys KC company

NPR editor resigns after writing piece critical of organization