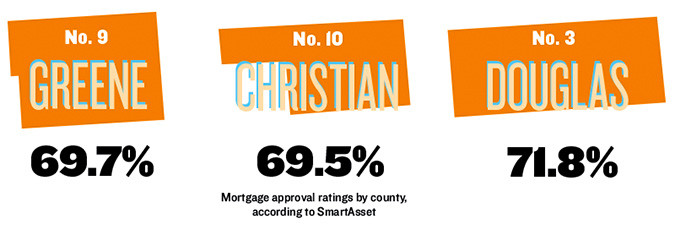

The American dream is a little easier to come by in Greene County than most areas of the country, according to a recent review of loan funding data.

With a mortgage-approval rating of 69.7 percent, SmartAsset ranked Greene County ninth in Missouri on its Loan Funding Rate list and No. 225 in the nation out of more than 3,000 counties. SmartAsset’s loan funding review, compiled with data from the Mortgage Bankers Association and the U.S. Census Bureau, is designed to determine the easiest counties for applicants to be approved for a home loan.

Douglas County earned the top local spot at No. 3 in Missouri with a 71.8 percent mortgage-approval rating, and Christian County landed at No. 10 with 69.5 percent in approvals.

Taking top ranks in the Show-Me State was Oregon County, in south-central Missouri, with a mortgage-approval rate of 74.2 percent. Clark County, in the northeast corner, rounded out the list at No. 115 with a 28.1 percent approval rate.

Keya Peha County, Neb., and Treasure County, Mont., topped the national list with 100 percent approval ratings. Kiowa County, Colo., bottomed out the rankings at No. 3,134 with a 14.7 mortgage-approval rate.

A.J. Smith, vice president of content for SmartAsset, said the company reviewed widespread loan-funding data to produce its Best Places to Get a Mortgage study. Smith said SmartAsset’s efforts did not focus on the contributing factors that led to the rates in individual counties.

“However, some factors that affect whether someone on an individual level gets approved for a mortgage include credit scores, income and employment,” Smith said via email.

Steve King, managing director of residential lending for Great Southern Bank, said the roughly 70 percent approval rate in Greene County was consistent with the bank’s rate across its Midwestern service area from Minneapolis to Fayetteville, Ark.

“We don’t deviate from that into the West or East coasts, which is where I think there is more deviation in approval ratings,” King said. “A lot of the markets we’re in are similar.”

Though SmartAsset doesn’t rank the states, its national review found approvals in the Midwest, West and Northeast were generally higher and loan-funding rates in the Southeast and Southwest were typically lower.

Also, approvals don’t tend to favor rural or urban markets in Missouri or across the nation, according to SmartAsset. With Great Southern covering both markets, King said loan programs through the U.S. Department of Agriculture and the Federal Housing Administration help level the playing field in rural areas with more traditional buyers in cities such as St. Louis, Kansas City and Des Moines, Iowa.

Volume in the Springfield market, according to King, was steady 2014-15 and through the first five months of 2016, but recent numbers are down from 2012-13 when refinances were booming. According to Springfield Business Journal archives, local mortgage volume for Great Southern – the local leader in mortgage loans on SBJ’s list – was valued at roughly $150 million in 2014 from over $220 million in 2013.

In recent years, King has noticed a shift to more new home or purchase loans. While both fall under the mortgage category, refinances usually are easier to turn around.

That shift is felt by Springfield Realtor Jim Hutcheson, who said he thought the local loan-approval rate might be higher than 70 percent. He has over 30 years of experience in real estate sales, and the past two years have been Hutcheson’s best yet.

“The market is as strong as I’ve ever seen it in terms of sales,” he said, noting his team at Jim Hutcheson Realtors is selling a few homes a week. “In the Springfield area, we’ve always had conservative bankers that don’t go too far out on a limb, but at the same time, they are aggressively making loans to first-time homebuyers and experienced homebuyers.”

Hutcheson said a stable local market and new interest from young professionals moving to the area could be part of the reason for the area’s higher than average approval rating.

One cause for concern for his company: Housing inventory is in short supply.

“We’d like to see more homes being built,” he said. “I’m seeing the homes sell quicker, and a lot of them.”

According to the Greater Springfield Board of Realtors – which oversees activity in Greene, Christian and Webster counties – the average time homes are on the market is falling. This year through June 2, homes in the three-county area spent 65 days on the market, which compares to 89 days during the same period last year. In May, the average was 52 days on the market, down from 74 a year earlier.

The demand is echoed across Great Southern’s footprint. This year, despite a roughly flat first five months, King projects at least a 5 percent bump in overall mortgages.

“I’m looking forward to summer and the end of the year as momentum grows behind the purchase market and more homes come online,” King said.

According to the most recent housing-starts data from the National Association of Home Builders, the annual rate of single-family starts in February was 822,000, up 37 percent from roughly 600,000 in the same month of 2015.

SmartAsset’s Best Places to Get a Mortgage study, which includes the loan-funding data, also factors five-year borrowing costs, property taxes and annual mortgage payments. With those criteria considered, SmartAsset ranked Greene County No. 25 in Missouri and No. 667 in the nation. On the best-places list, Oregon County again landed on top in Missouri. Locally, Stone County ranked third in the Show-Me State; Wright County was named No. 5; Douglas County was No. 9; and Webster County was listed at No. 10.